AI Financial Advice vs Human Financial Advisor: Why YouTube Advisors Should Be Celebrating

Executive Summary

I'm going to say something that will upset a lot of people who just spent the last two weeks panicking on LinkedIn: the ChatGPT–Plaid integration is the best thing that's happened to YouTube-first financial advisors in years. (I'll give you a moment to close your jaw.)

Here's what actually happened. ChatGPT Pro — that's the $200-per-month tier, not $20-per-month as the viral post claims — connected to 12,000 financial institutions through Plaid. It can read your bank balance. It cannot run a Monte Carlo simulation, execute a trade, owe a fiduciary duty, carry malpractice insurance, or sit across the table from a client who just found out their spouse has Alzheimer's. OpenAI's own disclaimer: "not a replacement for professional financial advice" (OpenAI, May 2026).

Meanwhile, the consumer trust data tells a story the doomsday crowd hasn't read. Only 38% of affluent investors are even comfortable with AI in their financial provider relationship — flat year-over-year (Cerulli Associates, 2026). A full 79% of investors with $250,000 or more would be upset if their advisor used AI without telling them (Janus Henderson, 2026). And 87% want a human element preserved regardless (Janus Henderson, 2026). The threat is real — but it targets advisors who offer nothing beyond commodity information. Advisors who've built trust at scale through YouTube? They're playing a different game entirely. This report gives you the data, the frameworks, and the case study evidence to understand why — and what to do about it using YT Era's Lighthouse Framework and Triple-A System.

The $200-Per-Month Dashboard That Broke the Internet (And What It Actually Does)

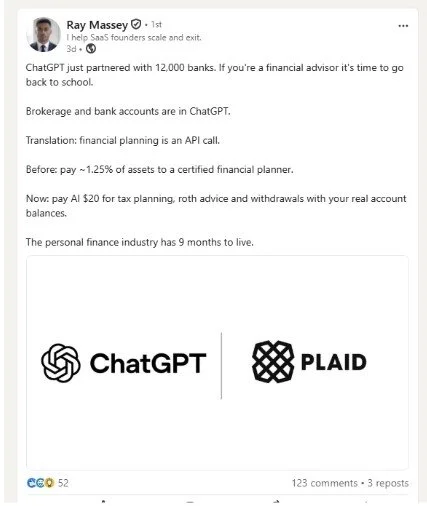

A LinkedIn post went viral the week of May 26, 2026. The claim: "ChatGPT just partnered with 12,000 banks. If you're a financial advisor it's time to go back to school." The prediction: "The personal finance industry has 9 months to live." The engagement: 52 reactions, 123 comments, and enough advisor anxiety to fill a therapist's waiting room.

Here's what the post got right: ChatGPT integrated with over 12,000 U.S. financial institutions via Plaid on May 15, 2026 (TechCrunch, May 2026). The integration uses GPT-5.5 and connects to banks including Schwab, Fidelity, JPMorgan Chase, Robinhood, and American Express (OpenAI, May 2026). Over 200 million users already ask ChatGPT financial questions every month (OpenAI, May 2026). And OpenAI absorbed the team behind personal finance startup Hiro in April 2026 — one month before the Plaid launch (TechCrunch, April 2026). This isn't a science experiment. It's a product strategy.

Here's what the post got wrong: the price. The Plaid integration launched on ChatGPT Pro at $200 per month — not the $20-per-month Plus tier (The Verge, May 2026). That's a 10x error in the most shared financial industry post of the week. (If your AI financial advisor can't get its own price right, maybe hold off on handing it your retirement portfolio.)

More importantly, here's what the integration cannot do. ChatGPT reads balances, transactions, investments, and liabilities through Plaid's OAuth scopes — specifically auth, balance, transactions, investments, and liabilities — but explicitly NOT payment_initiation (OpenAI technical documentation, May 2026). Translation: it can see your money. It cannot touch your money. It cannot execute trades. It cannot run Monte Carlo simulations modeling sequence-of-returns risk under regulatory compliance guardrails. It cannot perform tax-loss harvesting. It cannot accept fiduciary liability. It carries no malpractice or errors-and-omissions insurance for its outputs.

OpenAI's own disclaimer — verbatim — states: "ChatGPT can help you stay informed and feel more confident managing your finances, but it is not a replacement for professional financial advice" (OpenAI, May 2026).

Rachel Tobac, CEO of SocialProof Security, put the security concern bluntly: "People are trusting AI tools like they're a trusted fiduciary. Your trusted fiduciary is required to work in your best financial interest, whereas a large, cloud-based AI service provider is often creating their policies based on their own best interest (and not yours)" (CNN, May 2026).

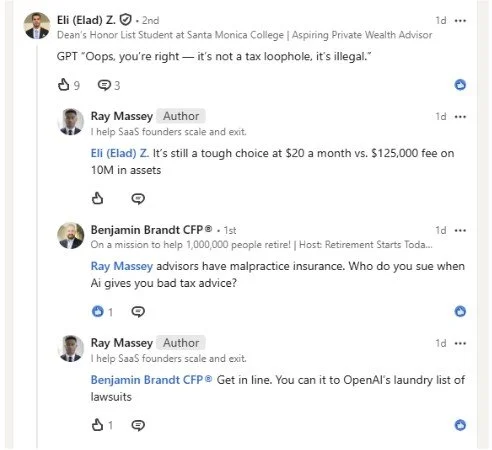

One commenter in the viral LinkedIn thread — Benjamin Brandt, CFP®, host of the Even Better Retirement YouTube Channel — crystalized the liability gap in a single question: "Advisors have malpractice insurance. Who do you sue when AI gives you bad tax advice?"

The best answer the AI-replacement crowd could muster? "Get in line. You can add it to OpenAI's laundry list of lawsuits." That's not a rebuttal. That's a concession.

And for the precedent-watchers: Schwab shut down Intelligent Portfolios Premium — its human-plus-robo hybrid advisory product — in early 2026. Michael Kitces characterized this as evidence of "how hard it is to offer low-cost advice to mass-affluent clients" (Kitces, January 2026). The robo-advisory model already tried to replace human advisors at the affluent tier. It didn't work. ChatGPT reading your checking account balance isn't a more compelling version of the same experiment.

What this is: a commodity-layer information tool. A dashboard. A very impressive dashboard — but a dashboard. What it is not: a fiduciary. A planner. A relationship. If you've been building any of those things through content, you should be smiling right now.

Apply to work with us HERE — YT Era helps advisors build the YouTube content system that makes commodity-layer AI competition irrelevant. When your prospects have watched you demonstrate expertise for months before they ever call, ChatGPT isn't your competition. It's the thing they used before they found you.

The Trust Data Nobody in the LinkedIn Comments Bothered to Read

The conversation about AI replacing financial advisors has a fatal flaw: it's happening almost entirely without data. Opinions are loud. Research is quiet. Let's fix that.

Three independent research organizations — surveying thousands of investors and U.S. adults in studies fielded between 2025 and 2026 — converge on the same conclusion.

Cerulli Associates (2026): Only 38% of affluent investors are at least somewhat comfortable with AI in their financial provider relationship. That figure is essentially unchanged from 39% in 2024 (Cerulli Associates, 2026). Among investors over 50 — the demographic that holds the overwhelming majority of investable wealth — comfort drops sharply: 42% for those in their 50s, and just 16% for those over 70 (Cerulli Associates, 2026). The people with the money don't want the robot.

Janus Henderson (March 2026): In a survey of 1,000 U.S. investors with $250,000 or more in investable assets, 79% said they would be upset if their advisor used AI without disclosing it (Janus Henderson, 2026). A full 85% believe the advisor is ultimately responsible for AI-generated advice and materials (Janus Henderson, 2026). And 87% want a human element preserved in the advisor relationship even if AI is used (Janus Henderson, 2026). Matt Sommer, Head of Specialist Consulting Group at Janus Henderson, summarized: "The demand for human-led decision making and personal connection will not be displaced by artificial intelligence; in fact, AI may actually increase the value investors place on those qualities" (Janus Henderson, 2026).

Gallup (April 2025): When asked where they get personal finance information, 41% of U.S. adults consult trained financial advisors and planners. Only about 20% each use podcasts, webinars, social media, books, or TV/radio (Gallup, 2025). Among adults 65 and older, 51% use financial professionals — the highest of any source for that age group (Gallup, 2025).

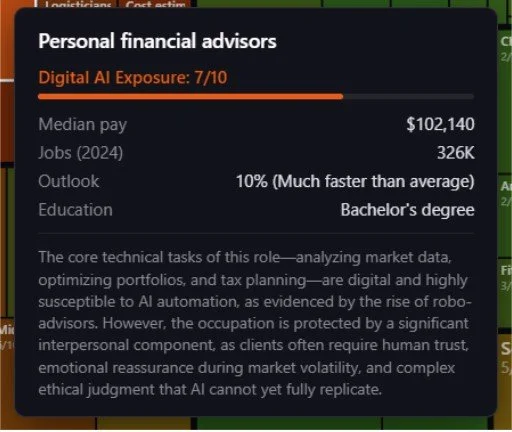

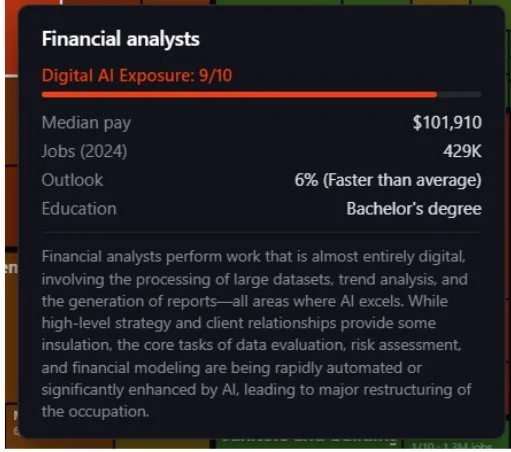

Now here's where it gets interesting for you, the advisor reading this report. Andrej Karpathy — founding member of OpenAI — built a tool that scored 342 BLS occupations for AI exposure on a 0-to-10 scale. Personal Financial Advisors scored 7 out of 10 (Karpathy, 2026). That sounds alarming until you see that Financial Analysts scored 9 out of 10 (Karpathy, 2026). Same industry. Radically different scores. The difference? Karpathy's own tool explains it: "The occupation is protected by a significant interpersonal component, as clients often require human trust, emotional reassurance during market volatility, and complex ethical judgment that AI cannot yet fully replicate" (Karpathy AI Exposure Tool, 2026).

Even the people building AI acknowledge the relationship moat.

And the relationship moat has a number. Russell Investments quantifies the total value a human advisor adds at 4.92% annually (Russell Investments, 2026). The largest component? Behavioral coaching at 2.30% — nearly half the total value, and the one capability AI is least equipped to replace (Russell Investments, 2026). Vanguard's "Advisor's Alpha" framework arrives at the same conclusion: behavioral coaching contributes approximately 150 basis points annually and is "the greatest potential value you can add" (Vanguard, 2022).

The Bureau of Labor Statistics projects 10% employment growth for Personal Financial Advisors from 2024 to 2034 — "much faster than the average for all occupations" — with approximately 24,100 openings per year (BLS, 2024). McKinsey projects a shortage of roughly 100,000 advisors by 2034 (McKinsey, 2025). J.D. Power's 2025 study found that 46% of current advisors plan to retire within 10 years (J.D. Power, 2025).

So: consumer trust in AI is flat. Investors overwhelmingly prefer humans. The BLS projects accelerating demand. The supply side is contracting. And the single most valuable thing an advisor does — behavioral coaching — is the thing AI is worst at.

If you're an advisor who has spent the last two years building a YouTube channel that demonstrates your expertise, your judgment, and your personality to thousands of prospects... you are holding the exact asset the market is about to pay a premium for.

This Week's Video Opportunities

The news cycle never sleeps, and neither should your content calendar. Here are two timely topics worth creating content around before they cool off.

1. "Trump Accounts and the New Estate Planning Window: What HNW Families Should Reconsider"

The Angle: The One Big Beautiful Bill Act established a $15 million permanent estate, gift, and GST exemption beginning in 2026 — indexed to inflation from 2027, with no sunset. Trump Accounts add a new savings vehicle for minor beneficiaries. Walk through what this means for multigenerational wealth transfer.

Target Audience: Families with $5M–$50M net worth; multigenerational HNW households

Why Now: Practitioners are working through implementation details. WealthManagement[dot]com published Christopher R. Hoyt's premium evaluation on May 21, 2026. Your audience is seeing headlines but doesn't have a trusted explanation yet. This window stays open 6–12 months.

2. "Social Security Trust Fund Now Projected to Run Dry in 2032: What Changed"

The Angle: The CBO's February 2026 update moved the OASI trust fund depletion projection to 2032 — one year earlier than the 2025 Trustees Report (CBO, February 2026). Without action, beneficiaries face an automatic estimated 7% cut in 2032 deepening to approximately 28% per year from 2033–2036. Reframe the claiming-strategy conversation.

Target Audience: Pre-retirees ages 55–72 with $1M+ in investable assets

Why Now: The timeline moved forward. Every pre-retiree in your audience needs an updated optimal claiming analysis. This topic has durable search volume and will remain relevant through 2026 and beyond.

Balance timely content with your evergreen library. The advisors who built multi-hundred-million-dollar practices created both.

Personal Brand Is the Empirically Proven Moat (And YouTube Is How You Build It)

The panic over AI in financial services rests on an assumption: that what clients pay for is information. If that were true, robo-advisors would have won a decade ago. They didn't. Schwab shut down its hybrid robo product in early 2026. The assumption is wrong. What clients pay for is trust — and trust is built through relationships, not through reading a bank balance. YouTube builds that trust at scale — and so does collaborative content with the CPAs and attorneys your clients already trust, as my report on COI collaboration content for financial advisors explored.

Brand Builders Group and the Center for Generational Kinetics conducted a Census-weighted national study of 1,005 Americans to measure exactly how personal brand affects consumer trust and purchasing behavior. The results: 74% of Americans are more likely to trust someone who has an established personal brand (Brand Builders Group, 2021). Among older millennials ages 35–44 — the cohort that is now reaching peak earning years and entering the wealth-management pipeline — that number rises to 85% (Brand Builders Group, 2021).

The profession-specific data is even more direct. 55% of Americans say it is important for their financial advisor to have an established personal brand — trailing only doctors at 61% and lawyers at 58% (Brand Builders Group, 2021). Among older millennials, 62% say it's important for their financial advisor specifically (Brand Builders Group, 2021). And 58% of Americans would pay more to receive services from a professional who does NOT work at a large company but has an established personal brand (Brand Builders Group, 2021). That last stat is worth reading twice if you're an independent RIA competing against wirehouses. The data says your independence is an asset — if you've built the brand to back it up. (The fact that this study was conducted before AI could read your bank balance makes it more remarkable, not less. If 55% wanted a personal brand from their advisor in 2021, the number today — when commodity financial information is literally free — is almost certainly higher.)

Wealthtender's 2025 Voice of the Client study analyzed 2,568 client reviews of over 200 advisors across 35 states. The finding: 89% of reviews focus on relationship quality, planning advice, and emotional factors. Only 10% mention investments or portfolio management (Wealthtender, 2025). Clients don't review their advisor the way they review a stock-picking algorithm. They review their advisor the way they review their therapist.

And the online research behavior data closes the loop: 96% of consumers will research an advisor online before making contact, even after receiving a referral (Wealthtender, 2025). Where will they research? 84% of U.S. adults use YouTube — the most widely used online platform in America, ahead of Facebook at 71% and Instagram at 50% (Pew Research Center, 2025). YouTube captures 13.4% of all U.S. TV viewing time — more than any other single media distributor in history, widening its lead over second-place Disney at 9.4% by 4.0 share points (Nielsen, 2025).

YouTube is a search engine, not a social feed. When a prospect types "should I do a Roth conversion before I retire," they're not scrolling. They're hunting. As my report on Roth conversion content that attracts $1M+ prospects documented, certain topics disproportionately pull affluent viewers into your funnel. And when they find an advisor who's published twelve hours of deep, specific, personality-driven content on exactly that question, they don't need ChatGPT to read their bank balance. They need your calendar link.

Root Financial demonstrates what this looks like at scale. James Conole built Root Financial Partners from startup to approximately $2.14 billion in assets under management with YouTube as the primary growth engine (SEC Form ADV, March 2026). The firm operates five YouTube channels with a combined footprint of approximately 298,000 subscribers, 4,702 published videos, and 49.4 million cumulative views (verified channel data, May 2026). Conole's production cost? Approximately $20,000 per year. His YouTube ad revenue? Approximately $120,000 per year — a net-positive marketing model (Brad Johnson, "Do Business Do Life" Podcast Ep. 062, May 16, 2024). The close rate from the first meeting after a prospect has consumed his content? "90%, 97% of people do move forward" — Conole's verbatim words (Brad Johnson, "Do Business Do Life" Podcast Ep. 062, May 16, 2024). The typical content-consumption period before a prospect reaches out? Approximately 18 months — based on a client telling Conole, "We've been watching your videos and your podcast for the last 18 months" (Brad Johnson, "Do Business Do Life" Podcast Ep. 062, May 16, 2024).

No chatbot generates an 18-month trust relationship. No dashboard produces a 90% close rate. No API call creates the parasocial familiarity that makes a prospect feel like they already know their advisor before the first meeting. As my analysis of YouTube Shorts strategy for financial advisors demonstrated, it's the deep, long-form content — not the sixty-second clip — that builds the kind of trust a $2-million prospect needs before handing over their life savings. And that's why the ChatGPT–Plaid announcement isn't a threat to advisors who've built this system — it's a competitive moat that just got wider.

Carroll Advisory Group provides a complementary proof point at a different scale. Devin Carroll has published 297 videos over approximately 11.5 years since launching his channel in October 2014 (verified channel data, April 2026). His channel has 477,000 subscribers and approximately 33.4 million cumulative views. The firm manages approximately $341 million in AUM across 279 client households, with an average client size of $1,222,430 (SEC Form ADV, April 2026). AUM grew approximately 50% in the past 12 months. That growth didn't come from a Plaid integration. It came from a decade of showing up on camera, being human, and building trust one video at a time — the kind of consistency my summer content strategy for financial advisors report is designed to protect during the months when most competitors go dark.

And for the enterprise-value angle: when PWL Capital was acquired by OneDigital in January 2025, Ben Felix's YouTube channel — 538,000 subscribers, 170 videos, 31.9 million views (verified channel data, April 2026) — was explicitly cited as a strategic asset in the acquisition. YouTube didn't just build PWL Capital's client base. It was explicitly cited as a strategic asset in the firm's acquisition. ChatGPT is many things. An acquirable business asset is NOT one of them.

When information becomes commoditized, the advisor who owns the trust relationship wins. The Lighthouse Framework positions your content as the signal prospects navigate toward in a sea of noise. The Triple-A System — Avatar, Authority, Ascension — is how you build the engine: attract the right viewer (not just any viewer), establish authority through demonstrated expertise, and create the strategic pathway that converts viewers into clients. My report on lead magnet strategy for financial advisor YouTube channels breaks down the Ascension layer specifically — the conversion mechanism that bridges the gap between "this video was helpful" and "I should fill out that form." Both of my frameworks position the advisor on the right side of the AI divide: using AI as an internal efficiency tool while building irreplaceable human connection through content.

Kitces captured the strategic irony perfectly: AI tools that eliminate entry-level advisor tasks may actually worsen the advisor shortage by collapsing the talent pipeline that trains the next generation (ThinkAdvisor, May 2026). The advisors who build personal brands now aren't just protecting themselves against AI competition. They're becoming more scarce — and more valuable — simultaneously.

73% of the advisors reading this will finish this paragraph and do nothing. (Source: my imagination, but the historical data on implementation rates makes it feel generous.) The other 27% will create a video this week.

Advisor Marketing Intel

YouTube Reaches 84% of U.S. Adults and Captures 13.4% of All U.S. TV Viewing Time

Pew Research Center's 2025 study of 5,022 U.S. adults confirmed YouTube is used by 84% of American adults — the most widely used online platform measured, ahead of Facebook at 71% (Pew Research Center, 2025). Nielsen's Media Distributor Gauge measured YouTube at 13.4% of all U.S. TV viewing time in July 2025, widening its lead over Disney by 4.0 share points (Nielsen, 2025). Why it matters: YouTube is no longer a "digital marketing channel." It is the dominant TV-room platform. Your HNW prospects are watching long-form content on 65-inch screens — and the production values, thumbnail readability, and sit-back viewing experience you deliver now determine whether they stay or scroll past.

Local SEO + AI Search Visibility Now Complements YouTube Discovery

At the 2026 Kitces Marketing Summit, Shaun Melby of Melby Wealth Management in Nashville presented a case study showing 25 qualified prospects per year for seven consecutive years through local Google and AI search optimization — closing approximately 10 new clients annually (Kitces Marketing Summit, 2026). Why it matters: all roads lead to YouTube. BrightEdge research analyzing citation patterns from May 2024 to September 2025 found that YouTube averages a 20% citation share across all major AI platforms — cited 200 times more frequently than any other video platform by ChatGPT, Perplexity, and Google's AI products (BrightEdge / Search Engine Land, October 2025). Google AI Overviews cite YouTube in 29.5% of results — the top domain overall, ahead of even Mayo Clinic at 12.5% (BrightEdge / Search Engine Land, October 2025). Your YouTube library isn't just a YouTube strategy. It's an AI-discoverable authority database. Every well-structured video on Roth conversions or estate planning becomes content that ChatGPT, Perplexity, Gemini, and Claude cite when prospects ask financial planning questions. YouTube is where they trust you. Google Business Profile and AI search are how they find you. And increasingly, AI chatbots are how they're sent to you.

FAQ (Or: Things You're Thinking But Too Polite to Say)

Q: But the price comparison — $200/month versus 1% of a $10M portfolio — doesn't that kill the traditional fee model?

A: On pure information, sure. $2,400 per year versus $100,000 per year is a 40x gap. But that comparison assumes what you're paying for is information — and the data says otherwise. Wealthtender's analysis of 2,568 client reviews found that 89% focus on relationship quality, planning advice, and emotional factors. Only 10% mention investments (Wealthtender, 2025). You're not competing with ChatGPT on information. You're competing on something it literally cannot offer: judgment, accountability, and a fiduciary obligation enforceable by law. Also, the $200-per-month tier doesn't even include the Plaid integration for Plus subscribers yet. So the comparison most people are making doesn't exist at the price point they're citing. (Details matter. Especially in financial services.)

Q: What about younger clients? Won't Gen Z and millennials just use AI?

A: Possibly for basic tasks — and that's fine. Over 60% of investors under 50 report comfort with AI (Cerulli Associates, 2026). But comfort with AI doesn't mean preference for AI over humans. When the Brand Builders Group study asked Americans whether it's important for their financial advisor to have an established personal brand, 62% of older millennials (ages 35–44) said yes (Brand Builders Group, 2021). And 68% of Gen Z would pay more for a professional with an established personal brand over one at a large company (Brand Builders Group, 2021). Younger clients don't want less human connection. They want a different kind of human connection — one that starts on YouTube, not at a golf outing.

Q: Should I be using AI in my own practice?

A: Absolutely — but for back-office, not for client-facing replacement. Schwab's study of 533 RIAs found 63% already use AI tools in some capacity (Schwab Advisor Services, 2026). J.D. Power reports 35% of advisors selected AI as the top priority for firm tech investment (J.D. Power, 2025). The winning strategy is AI internally for efficiency while amplifying the human relationship externally through content. Advisors who use AI to replace the relationship will trigger the 79% backlash Janus Henderson documented (Janus Henderson, 2026). Advisors who use AI to scale operations while building trust through YouTube will win both sides of the equation.

Q: Isn't "build a personal brand" just another way of saying "hope for the best"?

A: Not when the data says 74% of Americans are more likely to trust someone with an established personal brand (Brand Builders Group, 2021). Not when 96% of consumers research advisors online before hiring — even after a referral (Wealthtender, 2025). Not when Root Financial grew from startup to $2.14 billion in AUM with YouTube as the primary engine (SEC Form ADV, March 2026). Personal brand isn't hope. It's infrastructure — and infrastructure is built with systems, not good intentions.

Q: What if I'm wrong and AI really does replace advisors in nine months?

A: Then the BLS is wrong about 10% employment growth through 2034 (BLS, 2024). McKinsey is wrong about the 100,000-advisor shortage (McKinsey, 2025). Russell Investments is wrong about 4.92% annual human advisor value (Russell Investments, 2026). Cerulli is wrong about flat AI comfort at 38% (Cerulli Associates, 2026). Janus Henderson is wrong about the 87% who want human elements preserved (Janus Henderson, 2026). And OpenAI is wrong about its own product not being a replacement for professional financial advice (OpenAI, May 2026). That's a lot of wrong for a lot of very smart organizations. But sure — maybe the creator of a LinkedIn post with 52 likes cracked it (I'm not betting my business on that. Are you?)

Q: What should I actually do this week?

A: Create one video. Make it unmistakably human. That's the weekly challenge below.

Weekly Challenge

Create one video this week that demonstrates something AI cannot do — your personal take on a client situation, your emotional intelligence in action, your specific expertise applied to a real scenario. Title it: "Financial Advisor's Take on [Topic]." Make it unmistakably human. Show your face. Share your opinion. Reference a real conversation you had with a client (anonymized, compliance-approved). Let the viewer see the person behind the credentials. The advisors building the practices that survive AI disruption aren't the ones with the best algorithms. They're the ones their prospects already trust. One video. This week. That's the assignment.

Additional Resources (Because Knowledge Without Action Is Just Trivia)

Knowledge is power, but implementation is profit. Here are YT Era resources to accelerate your success (yes, we're shamelessly plugging our stuff… at least this stuff is FREE and we're honest about it):

The Part Where We Ask You To Do Something

If you've read this far, you understand something most of your competitors don't: the ChatGPT–Plaid announcement didn't make YouTube less important. It made YouTube the differentiator. When every advisor's client can ask a chatbot about their checking account balance, the advisor who has 18 months of trust-building content in front of every prospect isn't threatened. That advisor is irreplaceable.

The question is whether you're building that content system — or watching from the sidelines while someone in your market does.

Apply to work with us HERE — we build the YouTube content strategy, production workflow, and compliance framework that positions your practice on the right side of the AI divide. Not every advisor is a fit. We specifically work with growth-focused RIA owners who understand that YouTube is a search engine, not a social media hobby — and who want a system, not a shortcut.

Fair warning: we only work with advisors who are tired of pretending the pipeline will fix itself.

Disclaimer

This report is for educational purposes only and does not constitute financial, legal, or marketing advice. Results vary significantly based on implementation, market conditions, and individual circumstances. Past performance does not guarantee future results.

Any earnings or income statements are estimates based on documented case studies. Your results may differ substantially. Success requires consistent effort, strategic implementation, and ongoing optimization.

Before implementing any marketing strategies discussed in this report, consult with your compliance department or legal counsel to ensure alignment with your firm's policies and regulatory requirements.

Sources (For The Skeptics)

Because apparently "trust me bro" isn't a valid citation anymore:

Primary Research Reports:

Brand Builders Group / Center for Generational Kinetics. (2021). Trends in personal branding: National research study (n=1,005 U.S. adults, Census-weighted; MOE ±3.1 pp at 95% CI)

Cerulli Associates. (2026). Investor skepticism of AI in financial advice persists. Cerulli Edge—U.S. Retail Investor Edition, 1Q 2026

Gallup. (2025, May 13). Americans' financial advice rooted in people (n=2,036 U.S. adults; fielded April 2–15, 2025)

Janus Henderson. (2026, May 19). 2026 investor survey: Perspectives on AI (n=1,000 U.S. investors with ≥$250,000 investable assets; fielded March 5–24, 2026 by 8 Acre Perspective)

J.D. Power. (2025, July 15). 2025 U.S. financial advisor satisfaction study (n=3,698 advisors)

Nielsen. (2025, August 26). Media distributor gauge: YouTube captured 13.4% of all U.S. TV viewing time in July 2025

Pew Research Center. (2025, November 20). Americans' social media use 2025 (n=5,022 U.S. adults)

Russell Investments. (2026, April). 2026 value of an advisor study, 13th edition (total advisor value: 4.92%; behavioral coaching: 2.30%)

Schwab Advisor Services / Logica Research. (2026, January 22). Schwab advisor AI in action: AI's transformative impact on RIAs (n=533 RIAs; fielded October 7–26, 2025)

Vanguard. (2022, September). Putting a value on your value: Quantifying Vanguard Advisor's Alpha (Kinniry, DiJoseph, Jaconetti, Walker, Quinn)

Wealthtender. (2025). Voice of the client study (n=2,568 reviews across 200+ advisors)

Wealthtender. (2025, August). How Americans will choose financial advisors in 2026 and beyond (n=500 U.S. adults earning $100K+)

Case Study Sources:

Johnson, B. (Host). (2024, May 16). How a financial advisor used YouTube to generate $400M+ of AUM (Ep. 062) [Audio podcast episode]. In Do Business Do Life Podcast (James Conole interview; primary source for $120,000 ad revenue, $20,000 production cost, 90–97% close rate, 18-month content consumption)

Root Financial Partners, LLC. (2026, March). Form ADV Part 2A. U.S. Securities and Exchange Commission ($2,141,036,560 discretionary AUM; 858 client households)

Carroll Advisory Group, LLC. (2026, April). Form ADV Part 2A. U.S. Securities and Exchange Commission (CRD #334565; $341M AUM; 279 client households)

Industry Data:

Congressional Budget Office. (2026, February). Social Security trust fund baseline projections (OASI depletion projected 2032)

Karpathy, A. (2026, March). U.S. job market visualizer — digital AI exposure scores (karpathy[dot]ai/jobs; Personal Financial Advisors SOC 13-2052: 7/10; Financial Analysts SOC 13-2051: 9/10)

Kitces, M. (2026, May 15). How AI could worsen the advisor shortage. ThinkAdvisor

Kitces, M. (2026, January). Schwab Intelligent Portfolios Premium shutdown commentary. Kitces[dot]com

McKinsey & Company. (2025, February). The looming advisor shortage in U.S. wealth management (~100,000 advisor shortage projected by 2034)

U.S. Bureau of Labor Statistics. (2024). Occupational outlook handbook: Personal financial advisors (SOC 13-2052; 326K employed 2024; +10% projected growth 2024–2034; ~24,100 openings/year)

Platform and Technology Sources:

OpenAI. (2026, May 15). ChatGPT–Plaid integration announcement (12,000+ U.S. financial institutions; GPT-5.5; verbatim disclaimer: "not a replacement for professional financial advice"). Coverage: TechCrunch, The Verge, Engadget, Neowin, Bloomberg

The Verge. (2026, May). ChatGPT Pro pricing: $200/month

TechCrunch. (2026, April). OpenAI absorbs Hiro personal finance startup team

Tobac, R. (2026, May). SocialProof Security LinkedIn post and CNN interview on ChatGPT–bank integration security risks (CNN, May 13, 2026)

Kitces Marketing Summit. (2026). Shaun Melby case study: Local SEO + AI search visibility (Melby Wealth Management, Nashville; 25 prospects/year for 7 years)

BrightEdge / Search Engine Land. (2025, October). YouTube citation share analysis across AI platforms (YouTube averages 20% citation share; Google AI Overviews cite YouTube in 29.5% of results — top domain overall)