Roth Conversion Content: The Topic That Attracts $1M+ Prospects

Executive Summary

There's a reason the fastest-growing retirement-focused RIAs aren't talking about their Roth conversion content strategy at conferences. They don't want you to know it's the most underpriced client acquisition channel in financial services. (Read that sentence again. Slowly.)

Oak Harvest Financial Group in Houston grew from approximately $85 million to $936,945,775 in regulatory assets under management in roughly six years, with YouTube as the primary acquisition engine (Oak Harvest Form ADV Part 2A, December 31, 2024; Kitces Podcast #383, 2024). Their most-engaged topics, per founder Troy Sharpe's own disclosure on Kitces Podcast #383 (2024), include Social Security, tax planning, and Roth conversions. Their account minimum is $500,000. The math is not subtle.

This report breaks down why Roth conversion content disproportionately attracts $1M+ prospects, the specific Roth questions those prospects are searching on YouTube right now, the compliance guardrails that keep this content on the right side of the SEC Marketing Rule, and a script framework you can film next week. Usual warning: this topic is not a silver bullet. It's a magnet. You still have to show up.

Why Roth Conversions Pull Million-Dollar Prospects (And LinkedIn Doesn't)

Let's talk about who actually searches "Roth conversion strategy" on YouTube.

Not the 28-year-old asking whether to max her Roth IRA. Not the college student wondering what a Roth is. The viewer you're fishing for has three things: a large pre-tax retirement balance, a pending income event, and a sophisticated enough vocabulary to type the word "conversion" into a search bar. In plain English — this person is not searching for advice. They're searching for an execution partner.

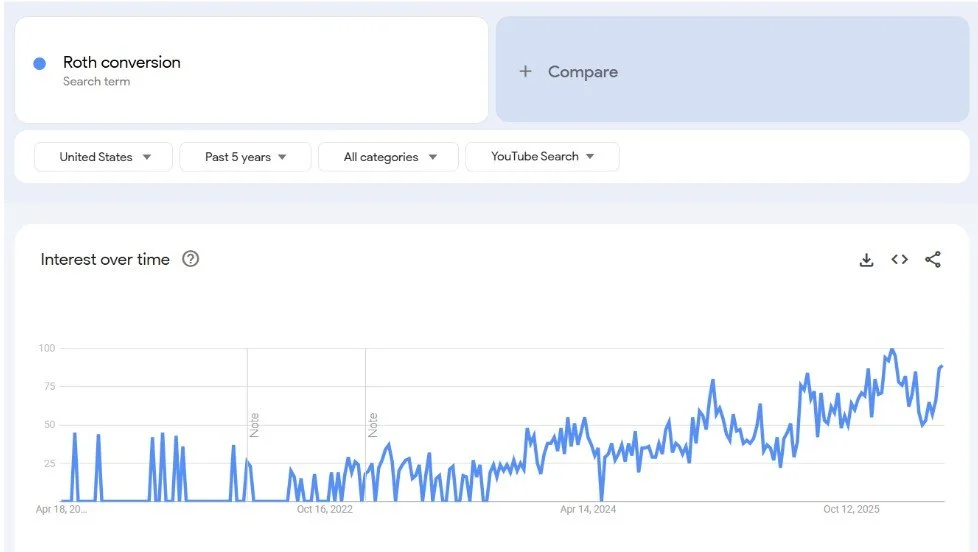

According to Google Trends data for YouTube Search in the United States (5-year window ending April 2026), search interest for "Roth conversion" has climbed from sporadic, low-level activity in 2021–2022 to sustained peak-interest readings in late 2025 and early 2026. Translation: this isn't a declining topic. The audience is getting bigger every quarter, and they're asking increasingly specific questions. (Specific questions from a sophisticated audience is, generally speaking, advisor heaven.)

Compare this to generic "5 retirement planning tips" content, which attracts everyone from 19-year-olds with student debt to 72-year-olds with $12 million. Your conversion rate from that audience is roughly the same as a billboard's. Technically non-zero, functionally embarrassing. (Source: my imagination, but any advisor who's ever tracked referral attribution knows exactly what I mean.) Roth conversion content inverts this — the keyword itself functions as a qualifier. The viewer has self-identified as someone with meaningful pre-tax assets, enough tax-vocabulary to type "conversion," and the cognitive bandwidth for a 20-minute educational video. Same filtering principle I detailed in my work on YouTube metrics that predict client acquisition.

The Oak Harvest case study makes this concrete. As of April 16, 2026, the primary @OakHarvestFinancialGroup channel has 59,400 subscribers, 555 published videos, and 23,874,257 cumulative views since joining May 23, 2019. The firm's $500,000 account minimum (per Form CRS and Form ADV Part 2A, 2025) filters the relationship. Their Roth conversion content filters the viewer. SmartAdvisormatch data (June 2025) shows 387 HNW accounts — approximately 42.81% of the client base. That's not an accident. That's what happens when every video is designed to be ignored by people who can't afford you.

Contrast the economics: social media marketing carries the highest client acquisition cost of any channel at $11,937 per client, while SEO/paid web listings deliver clients at $674 each — second only to client referrals at $338 (Kitces Research, 2019). YouTube content sits inside the SEO bucket, not the social media bucket, which is the entire point — YouTube is the world's #2 search engine, not a social feed. Roth conversion content on YouTube compounds indefinitely, attracts prospects who've already diagnosed their problem, and makes referrals easier because your existing clients and network can share a video that does the explaining for them. (I went deep on these numbers in a prior report on the real cost of each marketing channel.)

The Roth Questions Your $1M+ Prospects Are Actually Asking

Most advisors assume Roth conversion content is one topic. It's not. It's a cluster of distinct searches, each representing a different prospect segment at a different decision stage. The advisors pulling qualified leads at scale have mapped this cluster and produced content for each layer.

Here's the layered structure based on documented retirement-content YouTube channels in the YT Era Research Library.

Layer 1: Awareness searches. "What is a Roth conversion." "Roth conversion explained." "Roth IRA vs. Traditional." Early-stage viewers — often pre-retirees who've heard the term from a friend or CPA and want a primer. Heritage Wealth Planning's Josh Scandlen, CFP® has built a 9,722-video library across two channels (per channel pages verified April 16, 2026) using this layer as a long-tail SEO anchor. He literally wrote a book called The Tax Bomb In Your Retirement Accounts: How The Roth IRA Helps You Avoid It (Sustainable Wealth Series, 2018).

Layer 2: Strategic searches. "When should I do a Roth conversion?" "Roth conversion timing." "Roth conversion in down markets." These videos attract prospects who've moved past "what" and are wrestling with "when." Merit Financial's @MeritFinancialAdvisors channel — originally built by Safeguard Wealth Management before the firm was acquired by Merit in April 2025 — specifically cited "The Value of Roth Conversions During a Bear Market" as a signature topic (WealthManagement.com, April 2025). Safeguard had grown this channel to 67,000+ subscribers alongside $597 million in AUM across 543 clients in 16 states by the April 2025 acquisition; the channel (rebranded under Merit) has since grown to 73,500 subscribers as of April 2026 (PR Newswire, April 29, 2025; WealthManagement.com, April 2025; channel verification April 16, 2026).

Layer 3: Tactical searches. "Five-year Roth conversion rule." "Roth conversion and IRMAA." "How much should I convert?" "Roth conversion and Social Security taxation." Highest-intent searches in the cluster. A viewer searching "Roth conversion and IRMAA" is not browsing — they're a pre-retiree actively managing MAGI tiers, usually with seven-figure pre-tax accounts, often within 18 months of a conversion decision. These videos convert directly to consultation bookings.

Layer 4: Life-event searches. "Roth conversion after selling a business." "Roth conversion in the year of retirement." "Roth conversion and widow penalty." Rarer searches, highest dollar-weighted prospect quality. A viewer searching for the widow penalty is often 65+, recently single-filing, sitting on a pre-tax account that just became dramatically more expensive. They need execution. Fast.

The strategic insight most advisors miss: you don't produce one Roth conversion video. You produce a ladder — one video at each layer, each linking to the next. Oak Harvest's documented strategy, per Sharpe's Kitces #383 disclosure (2024), leans on the observation that retirement-age Americans became YouTube's fastest-growing user segment during COVID-19 and have sustained that behavior. They search, watch, and return. A ladder means they binge you, not your competitor. Every rung stays educational, not promotional — compliance framework in the next section.

If you're reading this and thinking "I know my next 12 videos should be about Roth conversions but I don't have the production bandwidth" — that's exactly the problem we solve. Apply to work with us and we'll tell you whether your practice is structured to benefit from a YouTube-first acquisition model.

This Week's Video Opportunities

Timely content works when it connects to planning decisions your HNW clients are already making. Here's what's hot this week that maps cleanly to your expertise.

1. "The Fed Just Paused With Inflation at 3.3% — What It Means for Your Bond Portfolio"

The Angle: Frame the post-FOMC landscape: March CPI came in at 3.3% annually, up from 2.4% in February (U.S. Bureau of Labor Statistics, April 10, 2026), and the Fed's late-April response sets the tone for bond duration, fixed-income allocation, and cash positioning through Q3. Stay on planning implications, not forward-looking rate predictions — compliance will thank you.

Target Audience: HNW pre-retirees with balanced portfolios; business owners carrying variable-rate debt or cash-equivalent reserves.

Why Now: Film the week after the April 29 FOMC meeting while the decision is still the dominant macro headline. 3–4 week relevance window before May CPI resets the narrative.

2. "The SEC Is Now Coming for Individuals, Not Firms — What That Means When You Hire an Advisor"

The Angle: Walk viewers through the SEC's FY2025 posture — 456 enforcement actions, approximately two-thirds with individual charges, a 27% YoY increase in individual accountability (SEC Newsroom, April 7, 2026). Frame as "what to ask your advisor" and why documented supervisory systems matter. Positions you as fiduciary-literate.

Target Audience: HNW clients evaluating a new advisor relationship; business owners who value institutional rigor.

Why Now: 30–60 day window; also works as an evergreen anchor.

Strike while the iron's hot on the first one — it'll feel stale fast. The second can stay in your library indefinitely. Timely content grows your channel this month; evergreen content pays your mortgage in 2028.

Compliance Guardrails: The Roth Content That Doesn't Get You in Trouble

This is the section most advisors want to skip. Don't.

Roth conversion content lives at the intersection of investment advice, tax advice, and planning guidance. It's useful precisely because it spans all three — which is exactly what makes it a compliance minefield without a framework. Here's the framework, which is simpler than your compliance team has made it sound.

Rule 1: Teach the math, not the outcome. The SEC Marketing Rule (Rule 206(4)-1 under the Investment Advisers Act of 1940) generally prohibits testimonials, performance claims, and projected-outcome language in advertising without specific disclosures. Translation: you can explain how a conversion interacts with marginal tax brackets, IRMAA, survivor-filing status, and RMDs. You cannot promise a viewer that converting $200,000 this year saves them $87,000 over their lifetime. (Yes, the math might actually say that. No, you can't say that in a public video without a mountain of context.)

Rule 2: Frame every video as planning education, not tax advice. Standard disclosure language for the intro or description: "This is educational content, not tax or legal advice. Your specific situation depends on facts I don't know. Consult your CPA and a licensed advisor before implementing any Roth conversion strategy." Not just liability insurance — a credibility marker. Sophisticated viewers recognize "consult your CPA" language as a signal that you're a real advisor, not a YouTube personality winging it.

Rule 3: Show the trade-offs, not just the upside. A Roth conversion always has a tax cost in the conversion year. Videos that show only future-tax savings get flagged for one-sided communication. Show both sides of the ledger, acknowledge when conversion doesn't make sense (for example, when the viewer's anticipated retirement bracket is lower than their current one), and let the viewer see you thinking like a planner, not a pitchperson.

Rule 4: Keep records and disclose conflicts. The Books and Records Rule (Rule 204-2) requires advisors to maintain records of advertising — save your scripts, descriptions, and claims. And if your firm earns an AUM-based fee while a Roth conversion temporarily reduces a client's pre-tax balance, acknowledge that conflict somewhere in your content library — typically once, in an evergreen "how we get paid" video linked from every other video. (Heaven forbid we make marketing boring, but compliance boring is the only kind that survives an exam.)

The advisors who get this right don't treat compliance as a constraint. They treat it as positioning. A video that says "here's the math, here's the trade-off, here's when it doesn't work, and here's what you should ask your CPA" is automatically more trustworthy than a competitor's "5 Roth Conversion Secrets The IRS Doesn't Want You To Know." One gets you clients. The other gets you an SEC comment letter. Run your framework past compliance before filming — most officers are more flexible on educational content than advisors assume, if the request arrives with structure attached.

Advisor Marketing Intel

YouTube Just Let Users Disable Shorts — The Platform Is Betting on Long-Form YouTube rolled out a zero-minute daily Shorts limit on April 15, 2026, letting users effectively remove Shorts from the dedicated tab and home screen on Android and iOS (The Verge, April 15, 2026). Why it matters: structural validation for long-form investment. When the platform itself builds a feature letting viewers opt out of short-form, it's signaling where long-term watch time is going. Roth conversion content — which needs 15 to 25 minutes to do justice — is aligned with platform direction, not fighting it.

The 2026 YouTube Algorithm Rewards Satisfaction + Segmented Content Practitioner analysis of the 2026 algorithm identifies audience satisfaction across a watch session — not single-video watch time — as the dominant signal, with retention best built around 3–5 distinct video segments, each opening with a micro-hook and closing with a payoff (iBuildInfluence, April 19, 2026). Why it matters: this maps cleanly to Roth conversion content, which naturally splits into layers (awareness, strategic, tactical, life-event). A single Roth video structured as 4 micro-segments — "what it is," "when it works," "when it doesn't," "how to decide" — is functionally a 2026 algorithmic cheat code.

LinkedIn Video Growth = Free Repurposing Surface for Your YouTube Library LinkedIn video uploads grew more than 20% in H1 2025, views up 36% YoY, 78% of B2B marketers now using LinkedIn video, and 71% of LinkedIn decision-makers are Gen Z/Millennial (Funnel.io, April 17, 2026). Why it matters: vertical and square clips repurposed from your long-form YouTube Roth videos have a warm, professionally-targeted distribution surface on LinkedIn. You don't need a LinkedIn-native strategy. You need a YouTube-first strategy with a 90-second repurpose workflow — roughly zero additional production hours.

Frequently Asked Questions (Or: Things You're Thinking But Too Polite to Say)

Q: What if I'm not a tax specialist? Can I still produce Roth content without overpromising? Yes — and honestly, you might be better positioned than the tax specialists, because your framing will stay on the planning side where the SEC wants it. You're not offering tax advice. You're explaining how Roth conversion interacts with a retirement income plan. Those are distinct activities, and the second one doesn't require a CPA after your name. It does require that you know your stuff — sophisticated viewers will catch errors faster than a junior associate at an audit firm.

Q: How long does it take for Roth content to start generating leads? Longer than you want. Root Financial's documented experience was that prospects consume 12–18 months of content before making contact (Kitces Podcast #445, 2025). Oak Harvest's ramp from $85 million to $936,945,775 took roughly six years (Kitces Podcast #383, 2024; Oak Harvest Form ADV, 2024). YouTube compounds. Paid ads don't. You're trading time for an asset you own versus time for traffic you rent.

Q: Won't my AUM book take a short-term hit if I encourage clients to convert pre-tax to Roth? Possibly — for 30 to 90 days while the conversion settles. Then the clients who noticed you put their outcome ahead of your short-term fee tend to send referrals for the next 20 years. If your compensation model is so fragile that optimizing for the client's after-tax outcome breaks it, that's a business model problem, not a content strategy problem. (Harsh. Also true.)

Q: Can I just have a ghostwriter or AI produce Roth content for me? You can have them produce drafts. You cannot have them be the face of the content. (To our knowledge, there isn’t a single successful case study of a Financial Advisor doing this - yet.) YouTube algorithmic weighting favors consistent creator identity — the same person, same setting, same framing over time. Viewers hiring you with $2 million want to know who you are. (Speaking of consistency — you can revisit that in my authority positioning framework.)

Q: I already have 40 videos on my channel and zero Roth content. Is it too late to pivot? No. The Google Trends YouTube Search curve for "Roth conversion" in the U.S. over the past 5 years is still climbing (Google Trends, April 2026). A 40-video channel with even 8 dedicated Roth ladder videos can meaningfully reshape the prospect mix coming through intake within 90 days. Start with one. Film it this week.

Q: Does the OBBBA permanent-lower-bracket environment change any of this? Yes, strategically. With lower brackets now permanent rather than set to sunset, the "convert now before brackets go back up" urgency has shifted. That doesn't make Roth content less relevant — it makes it more nuanced. The framing moves from "do it before brackets rise" to "when does conversion still pencil out given your specific income trajectory." That's exactly the question sophisticated viewers are asking in 2026. Answering it well is a direct path to the consultation booking.

Your Weekly Challenge

This week, film the first video in your Roth conversion ladder — a Layer 2 strategic video titled something like: "When Should You Consider a Roth Conversion (The Planning Framework, Not The Sales Pitch)."

Structure it in four segments, each with a micro-hook and payoff:

The one question to answer first (current vs. future marginal tax bracket)

The three windows when conversion mathematically favors most HNW retirees (early retirement gap years, market downturns, pre-RMD years)

The two situations when conversion is usually the wrong move (no tax diversification, planned charitable giving)

The decision framework: three numbers your advisor needs before the conversation happens

Keep it 12 to 18 minutes. Include the compliance disclaimer in the description. Close with "if you want to see the math on your specific situation, book a 30-minute planning meeting." Publish it. Then film the next rung. If you don't have a Layer 1 "what is a Roth conversion" video yet, film that one first — viewers rarely binge backwards.

Additional Resources (Because Knowledge Without Action Is Just Trivia)

Knowledge is power, but implementation is profit. Here are YT Era resources to accelerate your success (yes, we're shamelessly plugging our stuff… at least this stuff is FREE and we're honest about it):

The Part Where We Ask You To Do Something

Here's the tension every growth-focused advisor is navigating. You know content marketing is the path. You know Roth conversion content is the specific topic that attracts qualified prospects. You also know that "film a video this week" is the thing that gets pushed to next week, while your LinkedIn posts collect 14 likes from people who will never hire you.

We exist to collapse that gap. YT Era helps growth-focused financial advisors produce a YouTube content strategy that actually attracts $1M+ prospects — with the production workflow, compliance framework, and topic ladder built for your practice. We work exclusively with licensed financial advisors, RIAs, and CFPs.

Apply to work with us. We'll look at your practice, your current content footprint, and your growth targets, and tell you honestly whether YouTube is the right acquisition channel for you. We've told people "no" before. We'll tell you too if the fit isn't right.

Fair warning: we only work with advisors who are tired of pretending the pipeline will fix itself.

Disclaimer

This report is for educational purposes only and does not constitute financial, legal, or marketing advice. Results vary significantly based on implementation, market conditions, and individual circumstances. Past performance does not guarantee future results.

Any earnings or income statements are estimates based on documented case studies. Your results may differ substantially. Success requires consistent effort, strategic implementation, and ongoing optimization.

Before implementing any marketing strategies discussed in this report, consult with your compliance department or legal counsel to ensure alignment with your firm's policies and regulatory requirements.

Sources (For The Skeptics)

Because apparently "trust me bro" isn't a valid citation anymore:

Primary Research Reports:

Funnel.io. (2026, April 17). What you need to know about advertising on LinkedIn in 2026.

Google Trends. (2026, April). YouTube Search interest data for "Roth conversion," United States, 5-year window.

iBuildInfluence. (2026, April 19). YouTube algorithm 2026: More views consistently.

Kitces Research. (2019, August). Client acquisition costs for financial advisor marketing strategies. Kitces.com.

U.S. Bureau of Labor Statistics. (2026, April 10). Consumer price index — March 2026.

Wyzowl. (2026, January). State of video marketing report 2026.

Case Study Sources:

Kitces, M. (Host). (2024, April 30). Leveraging YouTube videos to organically grow 9x to $750M in just 5 years with Troy Sharpe (No. 383) [Audio podcast episode]. In Financial Advisor Success Podcast.

Kitces, M. (Host). (2025, July 8). Leveraging educational YouTube videos to drive hundreds of new clients per year with James Conole (No. 445) [Audio podcast episode]. In Financial Advisor Success Podcast.

Scandlen, J. (2018, July). The tax bomb in your retirement accounts: How the Roth IRA helps you avoid it. Sustainable Wealth Series, Book 2.

Industry Data:

PR Newswire. (2025, April 29). Merit Financial Advisors acquires Safeguard Wealth Management.

WealthManagement.com. (2025, April). Merit Financial acquires Safeguard Wealth Management.

The Verge. (2026, April 15). YouTube now allows you to disable Shorts.

Platform Documentation:

Oak Harvest Investment Services, LLC. (2025, August). Form ADV Part 2A brochure (reflecting December 31, 2024 period-end). U.S. Securities and Exchange Commission.

Oak Harvest Investment Services, LLC. (2025). Form CRS. U.S. Securities and Exchange Commission.

SEC Newsroom. (2026, April 7). SEC announces FY2025 enforcement results.

U.S. Securities and Exchange Commission. (2020, December 22). Rule 206(4)-1 under the Investment Advisers Act of 1940 (SEC Marketing Rule).

U.S. Securities and Exchange Commission. Rule 204-2 under the Investment Advisers Act of 1940 (Books and Records Rule).

YouTube channel verification: @OakHarvestFinancialGroup, @HeritageWealthPlanning, @JoshScandlen, @MeritFinancialAdvisors — subscriber, video, and view metrics verified by direct visual inspection, April 16, 2026.